The total amount of money in existence does not decrease, no matter how much is spent. If you spend 1,000 yen to buy a cake, 1,000 yen disappears from your wallet (and the cake disappears once eaten), but in exchange, the baker’s wallet grows by 1,000 yen. The total volume of money remains unchanged. Conversely, if you choose not to spend that 1,000 yen, the total supply doesn’t increase; the baker simply receives less. You might think your salary increases the money supply, but your company’s revenue ultimately originates from the funds of other firms or individuals—your employer isn’t “creating” new money.

However, statistics clearly show that the total money supply in circulation (Money Stock) increases over the long term. So, when is money actually created? It is private banks that directly increase the money supply through a mechanism called Credit Creation.

(The following diagrams were created with reference to Hayakawa, 2022.)

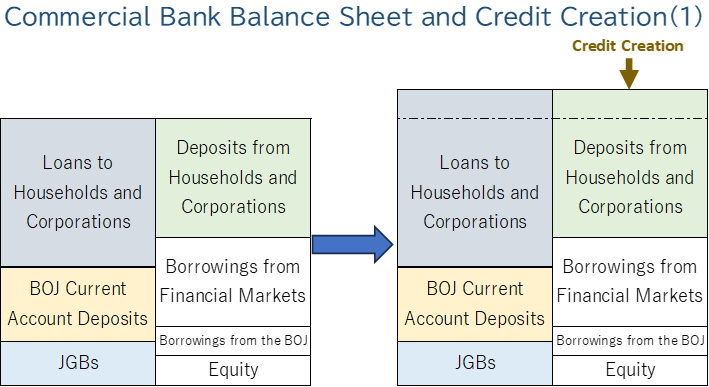

1. When Banks Increase Lending

When a bank increases its lending, it performs an accounting entry: it increases the deposit balance in the household or corporate account while simultaneously recording the loan as an asset. This is the quintessential act of credit creation. The bank is not taking physical cash from its vault and handing it over; therefore, the money in circulation increases at that moment. Put another way, a bank can increase lending—and thus create credit—even if its physical cash on hand is zero.

Conversely, when a corporation or household repays a bank loan, the money in circulation decreases.

Note: “Banks” here includes credit unions and other financial institutions with deposit-taking functions, but excludes life/non-life insurance companies and non-bank lenders that do not take deposits.

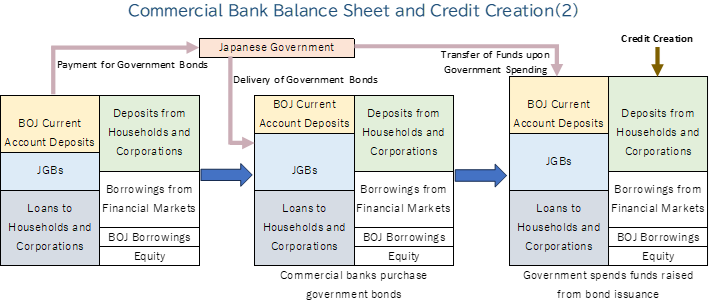

2. When the Government Increases Spending via Bond Issuance

While slightly different from typical bank lending, government spending is also considered a part of credit creation. When the government issues bonds to fund public works, commercial banks purchase the majority of them. At this stage, banks pay the government using their BOJ Current Account Deposits, shifting those assets into government bonds (JGBs).

When the government actually spends that money, it transfers funds into the BOJ current accounts of the commercial banks. The banks then increase the deposit balances of the companies that won the public works contracts (e.g., developers or advertising agencies). Again, no accounting process involves reducing physical cash on hand. This is how money enters circulation. Conversely, when government bonds are redeemed, the reverse mechanism occurs, and the money supply shrinks.

Monetary vs. Fiscal Policy

- Traditional Monetary Policy (manipulating short-term interest rates) targets the first function. To accelerate the economy, rates are cut to encourage borrowing; to cool it down, rates are raised to discourage it.

- Fiscal Policy is the second function in action. To stimulate the economy, bonds are issued to expand spending; to slow it down, bonds are redeemed to reduce spending.

Note that the BOJ current accounts, which initially decreased when bonds were issued, return to their original level once the government spends the full amount of the raised funds. Since the balance of BOJ current accounts does not change regardless of the scale of fiscal policy, those accounts do not act as a constraint on bond issuance.

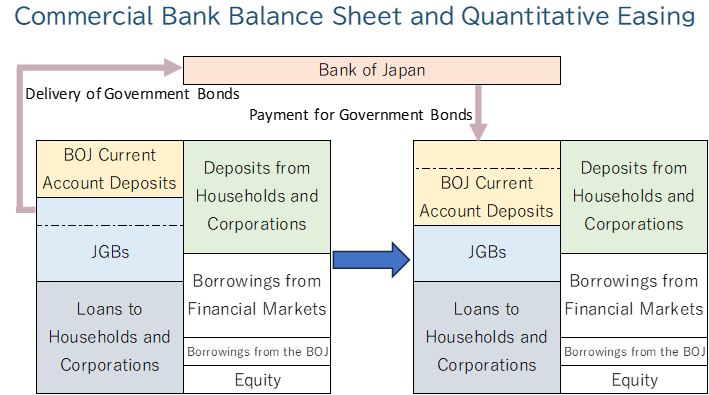

Comparison with Quantitative Easing (QE)

In QE, the Bank of Japan purchases government bonds. This increases the BOJ current accounts held by banks, but household and corporate deposits do not increase at all. Therefore, QE has no direct impact on the amount of money in circulation. However, it may indirectly increase the money supply through the first function (lending) by lowering medium-to-long-term interest rates.

Conclusion

Credit creation is the bedrock of MMT thinking (though actual MMT covers a much broader scope). I often see critics claiming that “MMT is a fantasy,” but if they are directing that criticism at the mechanism of credit creation, their argument makes little sense. Credit creation is a simple accounting fact describing how money increases; it is neither a policy nor an ideology.

References: Hideo Hayakawa (2022), The MMT School’s Understanding of Credit Creation: Contributions and Limits, Tokyo Foundation for Policy Research.

コメント